Rising rental costs and what they mean for UK hospitality

The UK hospitality sector is no stranger to change, but the current landscape feels different.

The reason is simple: the pressures that used to arrive one at a time are now happening all at once.

Since 2021, labour, food, energy, insurance, and taxation costs have all increased, often with little time between each rise. Instead of easing, these challenges have continued to overlap.

And into that already busy mix comes another factor: rising rental costs in hospitality.

For hospitality businesses already keeping a close eye on margins, higher rents add one more challenge to navigate. Understanding how this fits into the bigger picture is essential for keeping your margins afloat.

In this article, you’ll get a clear picture of how rising UK restaurant rents fit into the wider hospitality landscape and what to keep in mind as you plan for the future.

Setting the landscape: hospitality is already under pressure

Since 2021, the cost of labour, food, energy, insurance, and taxes has risen sharply. Here are a couple of examples:

- From July 2020 to 2025, food prices rose by around 37% – an increase of 4.4% from the previous five-year period.

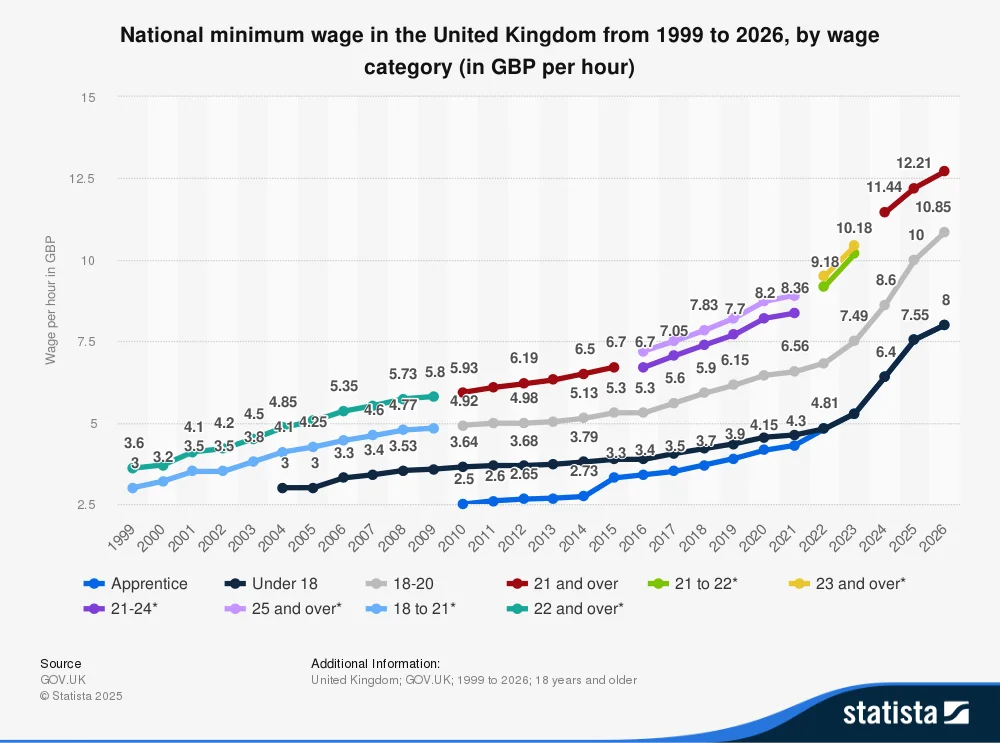

- In April, the minimum wage for people 25+ was £8.72. From April 2026, this will increase to £12.71 (+4.1% from the previous year) for those aged 21+. For employees aged 18- 20, this will increase to £10.85 (+8.5%).

These figures from Statista show the spike in labour costs over the last few years:

These increases leave operators with far less room to absorb unexpected shifts, like equipment breakdowns or changes in customer demand.

Many businesses are still managing pandemic-era debt on top of this, while post-inflation consumer behaviour means that customers are more selective with how and when they spend their money.

These challenges are showing up clearly in industry numbers:

- Licensed premises fell by 0.4% in the first six months of 2025, with 374 hospitality closures in the UK during this period. That equates to net closure of two venues per day.

- The sector is 14.2% smaller than it was in 2020.

Net closures continue across restaurants, pubs, and cafés, reflecting the strain of running sites with incredibly tight margins

It’s against this backdrop that rising rents are entering the picture. For operators already balancing higher costs, rental increases become one more pressure point in an already delicate financial equation.

What’s happening with commercial rents across the UK?

After several years of ups and downs, commercial rents in a lot of UK cities have started to stabilise. In May 2025, the average prime yield held at 5.91% for the third month in a row.

That said, rental costs are still considerably higher than they were before the pandemic. For hospitality operators, this means occupancy costs are top of mind.

Prime locations (think high streets and bustling city centres) are still commanding strong rents. Bond Street in London, for example, experienced a 20% increase in prime headline rents in 2024, making it the most ‘expensive’ retail street in Europe.

Secondary or suburban sites are seeing a more mixed picture, with some downward costs where demand is softer.

Landlords are also shifting rental terms. Shorter leases, more frequent rent reviews, upwards-only clauses, and rates-linked adjustments are becoming incredibly common.

Side note: Upward-only clauses ensure that rent only goes up over time, even if the market or business conditions change. Although there is talk of the UK Government cutting upward-only clauses for commercial leases, so watch this space.

While these measures make sense from a landlord’s perspective, they add a layer of unpredictability for operators.

Why? Because occupancy costs for restaurants may rise automatically without any direct action from the business.

To sum it up: Rents aren’t necessarily spiking everywhere, but staying on top of how they’re structured and where costs could escalate is crucial for managing margins effectively. It’s more important than ever to keep a close eye on leases and factor potential increases into financial planning.

London hospitality rents: the market behaving in its own orbit

London continues to stand apart from the rest of the UK when it comes to commercial hospitality rents, consistently ranking as the country's most expensive cities for leases.

Prime retail areas (think Bond Street, Soho, Covent Garden) have seen double-digit rent increases as international brands return and footfall recovers.

For F&B operators in central zones, this means:

- Intense competition for the most desirable units

- High premiums on corner or dual-frontage sites

- Rising service charges and insurance costs

- Strong landlord leverage thanks to tourism recovery and sustained retail demand

The picture changes slightly when you look at outer boroughs, but hospitality units generally continue to experience upward rent pressure. These rising costs are driven by strong local demand for neighbourhood cafés, pubs, and restaurants.

In other words, operators need to stay alert to rising occupancy costs no matter where they are.

The operational impact: how rising rental costs in hospitality affects P&L performance

For many hospitality businesses, rent typically makes up around 6-12% of total revenue, though this varies by concept and location.

When rents rise faster than income, it quickly starts to pinch the bottom line. Operators may notice tighter cash flow, lower EBITDA, less money for reinvestment, smaller staff incentives or training budgets, and even delays to expansion plans.

For operators with multiple sites, a rent increase at just one or two key locations can affect the finances of the whole estate. Upward-only clauses can make this even trickier, locking businesses into long-term rent rises that are hard to predict.

Keeping track of rent trends and how they interact with revenue is key to staying on top of margins.

Case examples: closures and pressure points across the UK

Across the UK, a number of hospitality closures have made headlines in recent years. Here are a couple of examples:

- One high-profile example is Greens, the vegetarian restaurant owned by Simon Rimmer. The Didsbury branch in Manchester closed in January 2024 after the landlord raised rent by around 35%, alongside significant increases in energy costs.

- In London’s Covent Garden, Petersham (which runs The Petersham restaurant and La Goccia) warned of potential closure due to a rent dispute with its landlord. The company filed a notice to protect itself while it tries to renegotiate.

Food for thought: It’s important to remember that rent alone is rarely the only reason a hospitality business closes. Although higher rent payments contribute to the problem, it’s the combined financial pressures of inflation across the board that push operators to breaking point.

Planning implications for operators

Rising rents don’t automatically put a business at risk, but they do require operators to stay proactive. The venues coping best right now are keeping a close eye on their occupancy costs and building smarter assumptions into their long-term planning.

A few areas are becoming especially important:

- Rent-to-turnover ratios. Checking this regularly helps you spot early signs of pressure and understand whether a site is still performing as expected.

- Business rates revaluations. Many operators now factor these into multi-year models rather than treating them as one-off surprises.

- Lease clauses tied to CPR or RPI. Agreements tied to CPI (Consumer Prices Index), RPI (Retail Prices Index) or fixed annual uplifts can change costs quickly. Knowing how these clauses escalate over time makes forecasting sales much easier.

- Service charges. In malls or managed developments, rising maintenance and utilities can lead to steep annual increases. Operators are watching these trends more closely.

- Scenario planning. Best-case, worst-case and neutral models build a realistic picture of how rent changes could affect margins – especially across multi-site estates.

- Estate mix. Some brands are balancing prime locations with steadier neighbourhood sites to keep overall occupancy costs in check.

When fixed costs climb, successful teams are also taking a closer look at the controllable parts of the P&L statement like labour deployment, food waste, and purchasing accuracy. It’s a natural way to protect margin stability when external pressures add up.

Looking ahead: what the next 12-24 months might hold

Looking forward, there are signs that the commercial property market (and by extension, hospitality occupiers) could see a more stable phase ahead:

- Stabilisation in some UK cities. According to Savills, prime high-street and shopping-centre rents are showing signs of recovery, with headline rents rising as vacancy stabilises.

- Strength in London prime sites. Savills’ research also suggests continued strength in top-tier London locations. Colliers backs this up, forecasting ongoing demand for the most coveted retail and hospitality spots.

- Potential softening in secondary or suburban retail. Savills warns that while prime areas are firming up, weaker locations may feel more downward pressure as pricing polarises.

- Turnover-rent structures may increase. With landlords and tenants looking for more flexible lease terms, more turnover-based rent deals are expected to emerge.

On the demand side, hospitality remains resilient. Even if costs are rising, operators are increasingly factoring occupancy costs (including future rent risk) into their expansion plans.

In practice, this means more careful site selection, tighter financial modelling, and scenario planning to protect margins.

All in, while the next 12-24 months won’t be entirely smooth, there’s a growing opportunity for operators who take a strategic, informed approach to their real estate footprint.

How Nory helps you control and manage costs

Rising rents and other fixed costs put pressure on margins, making it more important than ever to keep a close eye on the controllable parts of your business.

The good news is that with the right restaurant technology, you can track spending, profits, and your bottom line in real time.

Nory combines workforce management, inventory tracking, and sales performance in one platform, giving operators clear visibility across their estate. You can forecast labour needs, manage stock accurately, and spot inefficiencies in real time to protect margins.

Book a chat to speak with our team and see how Nory can tighten your cost control and protect margins as rents rise.